- +1 (845) 367-4240

- info@colonialpropertymanagement.com

- 410A New York 59, Airmont, NY 10952, USA

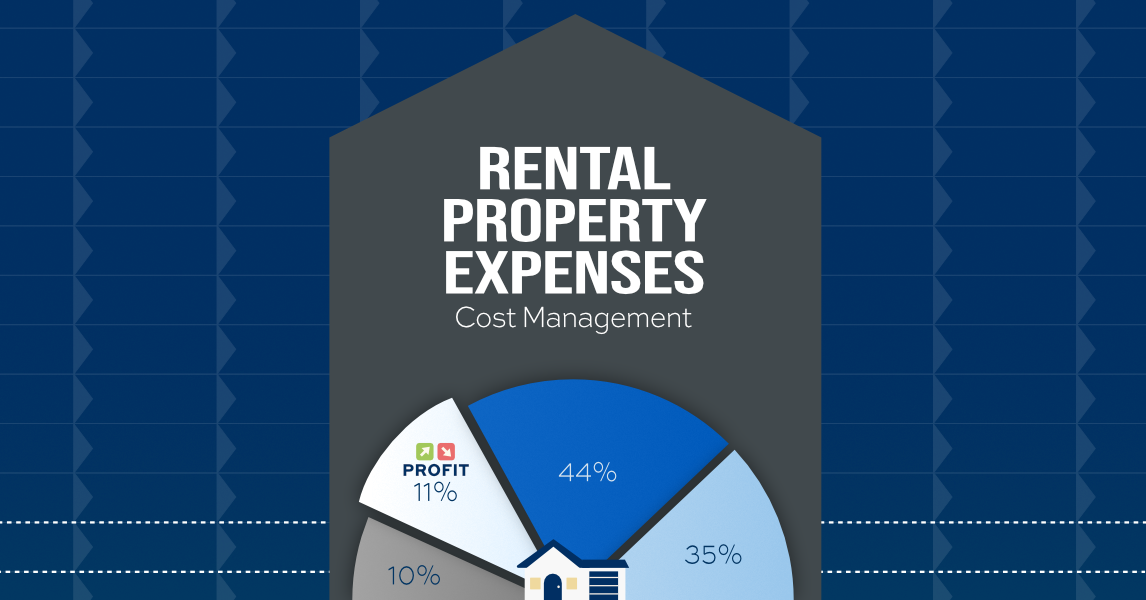

Every rental property is a business. Rental income comes in, and a portion of that revenue is consumed by property expenses each month. Operational costs are essential for keeping a rental running. But according to the National Apartment Association’s 2026 Dollar of Rent research, roughly 89 cents of every rent dollar goes to covering mortgage payments, taxes, maintenance, and other operating costs— leaving a surprisingly thin profit margin.

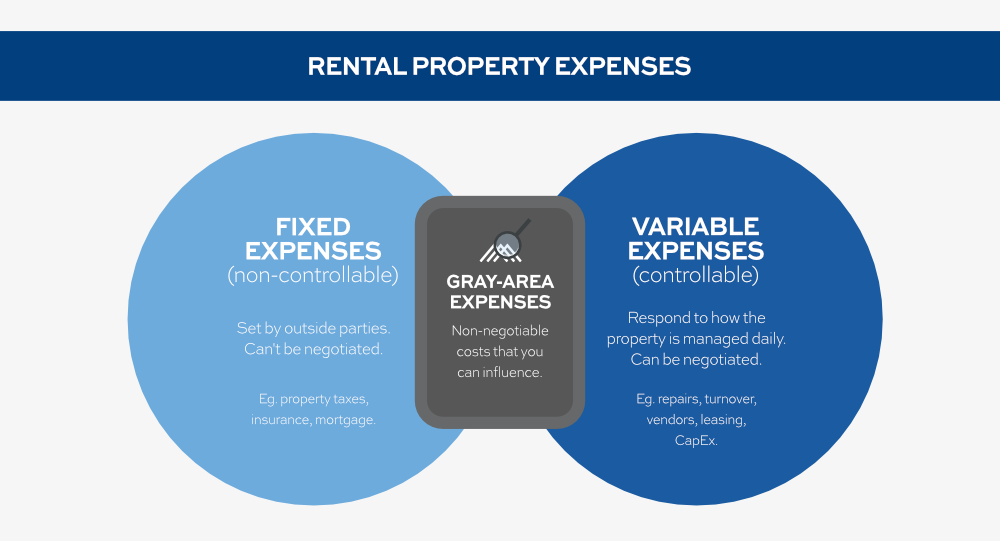

The good news? Not all expenses are created equal. When you examine your rental property expenses, you can categorize them into three types: the ones you control, the ones you can’t, and the ones that fall somewhere in between.

Cost optimization doesn’t come from scrutinizing expenses you can’t change. It comes from managing the ones you can. That is where your decisions directly influence net income and long-term return on investment.

This cost management framework helps you identify which expenses impact your returns and where good property management makes a difference.

Some expenses are set by outside parties — local government, lenders, insurance carriers. You don’t negotiate these line items. But you need to know what you are paying for, whether the amount is accurate, and when an incorrect assessment or billing error is worth disputing.

Property taxes are the single largest operating expense on a rental property. They consume 25–35% of total operations costs. In Goshen, NY, and across Orange County, the effective rate is 2.59%. That’s more than two and a half times the national median of 1.02%. For every dollar you spend on property expenses, roughly a quarter to a third goes straight to the tax bill.

And that bill can change. A new assessment, a school budget adjustment, or a shift in municipal levies can all push your taxes higher, even if your property’s market value hasn’t changed. What you paid last year isn’t what you’ll necessarily pay next year.

You can’t negotiate the tax rate. But you can verify that your assessment is fair. A professional management team can review your numbers, flag an over-assessment, and help you file a grievance if the valuation looks inflated. One practical step: pull your latest assessment and compare it to recent sales nearby. If your number looks high, a grievance may be worth your time.

In New York, landlord insurance typically costs between $300 to $950 per month depending on building size, age and location. While New York doesn’t legally require it, most lenders do.

This is one of the fastest-rising costs in property ownership right now. Weather claims, repair costs, and stricter underwriting are all pushing rates up. Premiums in New York climbed 13% between 2021 and 2024, according to the Consumer Federation of America, even as coverage in many cases has not expanded.

Premiums aren’t directly negotiable, but a property’s claims history, maintenance records, and system updates can influence underwriting decisions. Property management companies often maintain this documentation as a matter of course. They may also have relationships with insurance brokers who work with rental portfolios, providing access to pricing structures not typically available to individual owners.

Rates on rental property mortgages run higher than owner-occupied loans. Lenders view tenant dependent income as a risk, so they charge a premium, and qualification standards are stricter.

In January 2026, a LendingTree analysis found the typical monthly mortgage payment nationwide was 37% higher than the median rent — a gap of roughly $548 per month. For many properties, rental income doesn’t fully cover the debt. That puts pressure on occupancy and on-time rent collection.

The payment itself is non-negotiable. What you can protect is the income stream that services it. Ensuring the mortgage gets paid on time means prioritizing consistent occupancy and predictable rent patterns. At the same time, using a Tenant Predictability Index can help anticipate tenant behavior and reduce turnover risk, therefore servicing debt.

These are the expenses where your decisions directly shape the margins of your profit. Unlike property taxes or mortgage payments, controllable costs respond to how the property is managed daily. The right approach reduces them.

Maintenance and repairs are one of the largest controllable line items for any owner. Industry-wide, these costs represent 15–20% of total operating expenses, and are projected to rise 5.7% in 2026, according to the Triangle Apartment Association’s 2026 analysis. Additionally in New York that ratio can skew higher, driven by the region’s older housing stock and harsh winter conditions.

Not all maintenance spending is equal. Emergency repairs cost 3 to 5 times more than planned work, creating a gap that separates reactive from proactive maintenance.

The best way to diagnose whether your budget is being drained by reactive spending is to calculate your Maintenance Burn Rate. A high burn rate signals that your property is being maintained in poor condition. Shifting from reactive to proactive spending is one of the most direct ways to improve net operating income without raising rents.

Vacancy comes in two forms. Physical vacancy is the percentage of units sitting empty. Economic vacancy is the revenue lost to concessions, debt, and non-payment from occupied units. Turnover is the expense that follows when a tenant leaves and the unit is made ready for a new lease.

For multifamily markets with tight vacancy rates, the problem isn’t empty units. When facing a housing shortage, your revenue isn’t lost to physical vacancy. A property with a 5% physical vacancy can have significant rent concessions and tenant debt, leading to an economic vacancy of 10% or more.

The way to control both types of vacancy and turnover is through better tenant screening, tenant retention, and renewal strategies. When turnover does occur, a streamlined process to prepare the unit and a pipeline to acquire qualified tenants will shorten the gap between move-out and move-in. Ultimately, good tenant management helps control your primary source of revenue.

Contract services cover the work you hire out: landscaping, snow removal, pest control, cleaning, and any specialized maintenance you don’t handle in-house. Vendor management is how you select, negotiate with, and hold those providers accountable. Both are controllable because the scope, the rate, and the performance standard are all yours to set.

Managing your vendor network well reduces overall maintenance costs. That means pre-negotiating rates, setting a clear scope, and evaluating workmanship. In the New York Tri-State area, winter weather is unpredictable. During a harsh winter season, what you spend depends directly on the choices made before the season starts.

Strengthening your vendor network, assessing quality and fair pricing, and evaluating what your properties actually need is what ultimately optimizes costs in this line item. Last winter, snow totals ran 40% above normal and per-push rates spiked 20–30%. That evaluation delivered 21% average savings across our Middletown clients.

Administrative and legal expenses cover the paperwork and processes that keep a rental property compliant: lease preparation, tenant screening, accounting, and recordkeeping. When something goes wrong, legal costs add to the bill.

In 2025, only half of the eviction proceedings in New York State resulted in a warrant, and many of those warrants were never executed. Statewide, 192,572 eviction filings resulted in just 95,820 warrants. When a Good Cause Eviction case fails, it’s usually because the filing wasn’t compliant or the tenant’s procedural protections were stronger than anticipated. Every eviction takes months. A failed case means court costs, attorney fees, lost rent, and potentially re-filing from the beginning.

Good tenant screening and thorough documentation reduce legal and turnover costs. Screening filters out high-risk tenants before they ever occupy a unit. Clear communication prevents disputes from escalating. And when removal becomes necessary, well-maintained records provide the leverage to pursue it.

Marketing and leasing expenses cover the costs of advertising vacant units, showing the property, and signing new tenants. But the most cost-effective way to control them isn’t spending more on new leases. It’s investing in tenant retention and long-term advertising channels.

The numbers back this up. According to Tellus, a new lease typically costs 50–100% of one month’s rent, while a renewal runs just 25–50%. In the Hudson Valley, professional management fees that include leasing run 8–10% of collected rent. You pay one bundled rate instead of absorbing a separate leasing commission every time a unit turns.

Beyond retention, the right marketing mix can lower costs further. An optimized Google Business Profile and website that ranks for local searches, a resident referral program, and a retargeting ad campaign that only reaches people who have already shown interest: all of these reduce reliance on paid listings and keep leasing costs predictable over time.

Capital expenditures are major, non-recurring repairs and replacements that extend the useful life of a property: a new roof, an HVAC system, a full repaving. Unlike daily maintenance costs that fall under OpEx, CapEx is infrequent but substantial. The expense itself is predictable; the surprise comes when maintenance is deferred and capital expenditures go unplanned.

Large numbers demand planning. Set aside 10–20% of annual NOI for capital reserves, per InvestWithCarbon. Across New York State, maintenance costs climb each year—a signal that owners are deferring maintenance and letting unplanned CapEx bleed into operating budgets. When you defer replacing major systems on a schedule, they generate repeated repairs and inflate operating costs.

CapEx is controllable because you can plan it 5 to 10 years in advance. Professional management maps the condition and lifespan of major property systems onto a replacement calendar. Monthly reserve contributions are set according to the property’s actual age and condition. This results in a planned HVAC replacement that strengthens the property’s value and prevents emergency maintenance.

Some expenses fall into both categories. Part of the cost is non-negotiable and set by an outside institution. The rest responds to how you manage the property. The point isn’t to eliminate these costs; it’s to target what you can control and influence your NOI over the long-term.

Utility costs span between fixed rates and variable usage. The rate is set by the provider and approved by the state, making it non-negotiable. But the amount of energy, water and fuel the property consumes depends on system efficiency, tenant behavior and how the bill is structured.

In New York, electricity costs 28.37 cents per kilowatt-hour, 62% above the national average and climbing since 2019, according to Empire Center. Water and sewage costs have also risen steadily. When utility bills spike, tenants often fall behind on rent. That’s why many multifamily owners cover water and sewer themselves: consumption is less variable than electricity, resulting in a more predictable cost to absorb while keeping rent stable.

Even when the rate is out of your hands, the usage is not. To manage consumption costs, the best methods are to structure billing around actual usage, plan energy-saving upgrades, and schedule seasonal maintenance. These steps keep consumption under control, even while rates keep rising.

Property management fees are monthly costs of professional management covering rent collection, tenant communication, maintenance coordination, financial reporting, and legal compliance. The fees depend entirely on the company, but you choose the manager. The rate becomes negotiable through comparison, and the decision is reversible if service falls short.

Professional management fees typically run 8–12% of gross monthly rent. The fee alone isn’t enough to know what the service returns. Self-managed properties carry 15–30% longer vacancy periods than professionally managed ones, and owners pay 15–25% more per repair without negotiated vendor rates. Professional management doesn’t eliminate costs, but converts them into a property expense you can evaluate and control.

A professional manager shortens vacancy by leasing faster. Preventive programs and vendor relationships drive down maintenance costs. Responsive communication keeps tenants renewing. And deep knowledge of local regulations helps you avoid legal exposure. Results show up across your portfolio as tighter vacancy, lower repair spending, and steadier NOI over time.

Yes. Property management fees are a standard operating expense and must be subtracted from revenue when calculating net operating income.

These fees, usually 8–12% of collected rent, cover day-to-day tasks such as tenant communication, maintenance coordination, and rent collection. Including them in your OpEx gives you an accurate, real-world picture of your property’s profitability.

A well-managed multi-family property typically runs an operating expense ratio of 35–45%, yielding an NOI of 55–65%.

Class A properties often operate closer to 30–35% expenses, while older Class C buildings may reach 45–55%. A ratio significantly outside these ranges usually signals controllable issues like high vacancy, deferred maintenance, or poorly negotiated vendor contracts.

They focus on two levers: increasing effective revenue and controlling operating expenses.

Revenue grows through strategic upgrades, ancillary income from pet fees or parking, and market-aligned pricing. On the expense side, preventative maintenance, annual insurance reviews, and pre-negotiated vendor rates keep costs in check, while strong tenant screening and retention incentives reduce turnover—one of the largest avoidable expenses.

It makes sense to switch when the cost of your time, stress, or mistakes exceeds the typical 8–12% management fee.

Common tipping points include owning more than three or four units, living out of state, or having a full-time job that leaves no room for tenant calls and maintenance. If your rental feels like an unpaid second job, a professional manager can turn it back into passive income.

Important Note: This post is for informational and educational purposes only. It should not be taken as legal, accounting, or tax advice, nor should it be used as a substitute for such services. Always consult your own legal, accounting, or tax counsel before taking any action based on this information.