- +1 (845) 367-4240

- info@colonialpropertymanagement.com

- 410A New York 59, Airmont, NY 10952, USA

Cash accounting records income when you receive it and expenses when you pay them. Accrual accounting records income when it is earned and expenses when they are incurred. In 2026’s selective market, demonstrating sustainable income starts with your accounting method.

According to Northmarq’s 2026 multifamily article, capital is active but highly selective. Their report notes:

“Buyers are rewarding expense control that reflects today’s cost environment, proactive maintenance that reduces execution risk, and conservative rent assumptions that can hold up under scrutiny.”

What does this have to do with accounting? Everything.

A buyer cares about what they can see. An accrual accounting method surfaces the deferred maintenance, the rent concessions, and the true expense trends that cash statements often hide. Knowing which accounting method to choose, between accrual vs cash accounting, can directly affect how your buyers and lenders value your property, helping you decide if it’s time to sell or refinance.

Cash accounting is a straightforward method. You log rent payments the day the check clears. You record a repair bill the day you pay the contractor. The numbers in your bank statement directly reflect your books.

This is the best method for an owner with a single rental property who plans to hold it long-term and never sell. Its simplicity helps small landlords track their money for tax purposes.

Example: A tenant pays January rent on February 2nd. This late payment will show an empty January and a much fuller February in your books. A major repair billed in December but paid in March hides the true cost of operating your property during the winter season.

Cash accounting records expenses on the payment date, not the date the work was done. This can understate the true cost of maintaining your property in your monthly reports.

Accrual accounting matches income and expenses to the period they belong to. January rent belongs in January, even if the tenant pays late. A December repair bill belongs in December, even if you pay the contractor in March.

This method provides a clearer picture of your property’s financial health because it records activity when it happens, not just when cash moves.

Here are four things that would be missing in your reports without accrual accounting:

For owners with multiple properties, accrual accounting lets you compare performance across your holdings. Cash accounting can make one building look stronger simply because a tenant paid early or a repair bill hasn’t cleared. Accrual accounting removes those timing differences, so you know which assets are truly performing.

Your accounting method determines what a buyer or lender sees when they review your financials. Accrual accounting ensures your financials match what they are looking for. It demonstrates revenue consistency and removes guesswork from a buyer’s valuation.

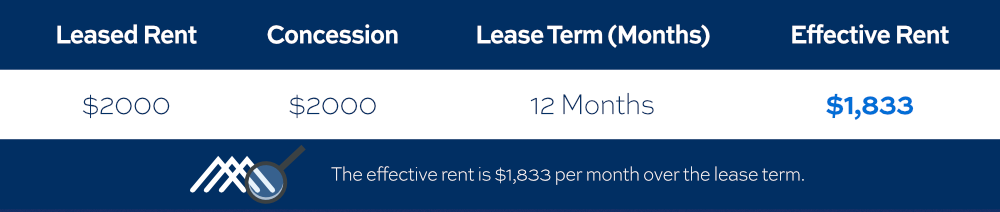

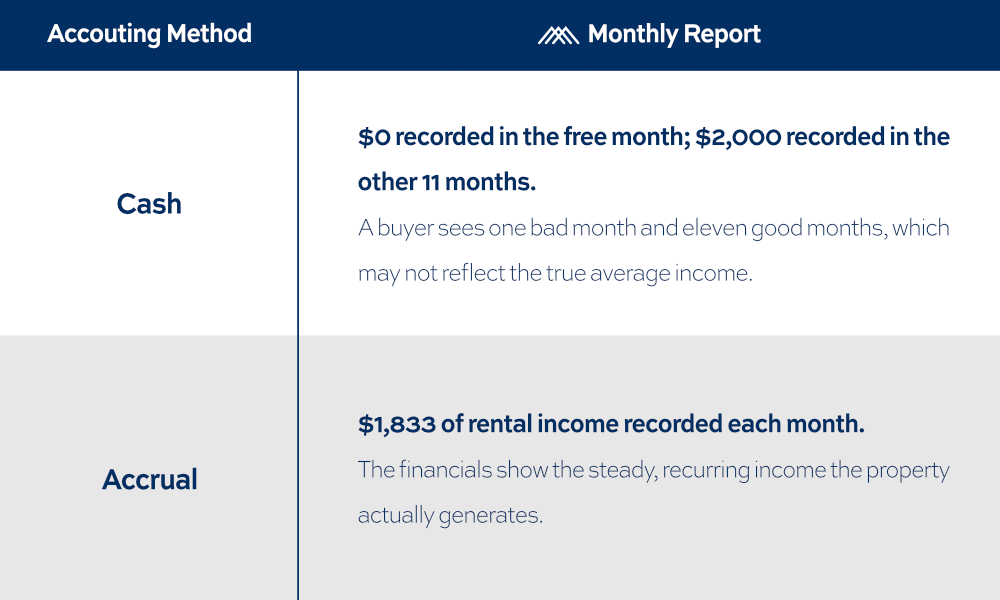

In 2026, over 41% of multifamily properties nationwide offer rent concessions like “one month free.” Under cash accounting, a free month shows as a sudden income gap. Under accrual accounting, that concession is spread evenly over the lease term, revealing the true effective rent of your property.

Underwriting concessions correctly means amortizing the concession value over the full lease term to arrive at effective rent. Instead of letting a free month create a misleading income gap, you calculate the average monthly rent the lease actually generates. Here’s how that same lease looks under cash accounting versus the more accurate accrual method.

Paylode’s 2026 analysis states that “asset attractiveness is defined by revenue quality, consistency, and confidence in future performance.” Accrual accounting directly supports this by spreading concessions evenly, presenting stable revenue. Cash accounting, by contrast, can make a well-performing property look unstable to a buyer.

In the New York and Connecticut markets, institutional lenders, agency financiers, and experienced buyers expect to see accrual-basis financials. GAAP-compliant reporting uses accrual accounting, and many federal lending programs require it. While a private sale might not demand accrual-basis records, preparing them keeps you ready for a wider range of offers.

For a more detailed discussion of these requirements from a top national CPA firm, see Aprio’s guide to GAAP vs. Tax Basis reporting.

Most small landlords use cash accounting for its simplicity. Larger portfolios and institutional investors operate on accrual accounting for its accuracy and because lenders require it.

Our property management services track accounts receivable, accounts payable, and provide monthly financial reports for owners across Rockland, Orange, Dutchess, Westchester, and the surrounding New York and Connecticut counties. We handle the day-to-day tracking so your books stay organized and ready for whatever your portfolio requires next.

For most individual landlords in New York, accrual accounting is not required for tax filing. You can use the simpler cash method as long as you qualify as a small business taxpayer under IRS rules. A CPA can confirm what applies to your specific situation.

For a multi-family portfolio, accrual accounting is the industry standard. It matches income and expenses to the period they belong to, giving you an accurate view of performance. Most lenders and buyers also expect accrual-basis financials when you seek financing or prepare to sell.

Yes. Many owners use cash accounting for tax filing and accrual accounting for internal management reports. This gives you the simplicity of cash for taxes and the accurate performance tracking of accrual for running your property. A CPA or bookkeeper can help you manage both sets of records.

The primary difference is timing. Cash accounting records income and expenses only when money changes hands. Accrual accounting records them when they are earned or incurred, even if payment happens later. Accrual gives you a more accurate long-term view of your property’s financial health.

Important Note: This post is for informational and educational purposes only. It should not be taken as legal, accounting, or tax advice, nor should it be used as a substitute for such services. Always consult your own legal, accounting, or tax counsel before taking any action based on this information.